Pay yourself optimizer

Salary or dividends from your Estonian OÜ? Compare four payout strategies side by side — total tax, company cost, health insurance and pension cover included.

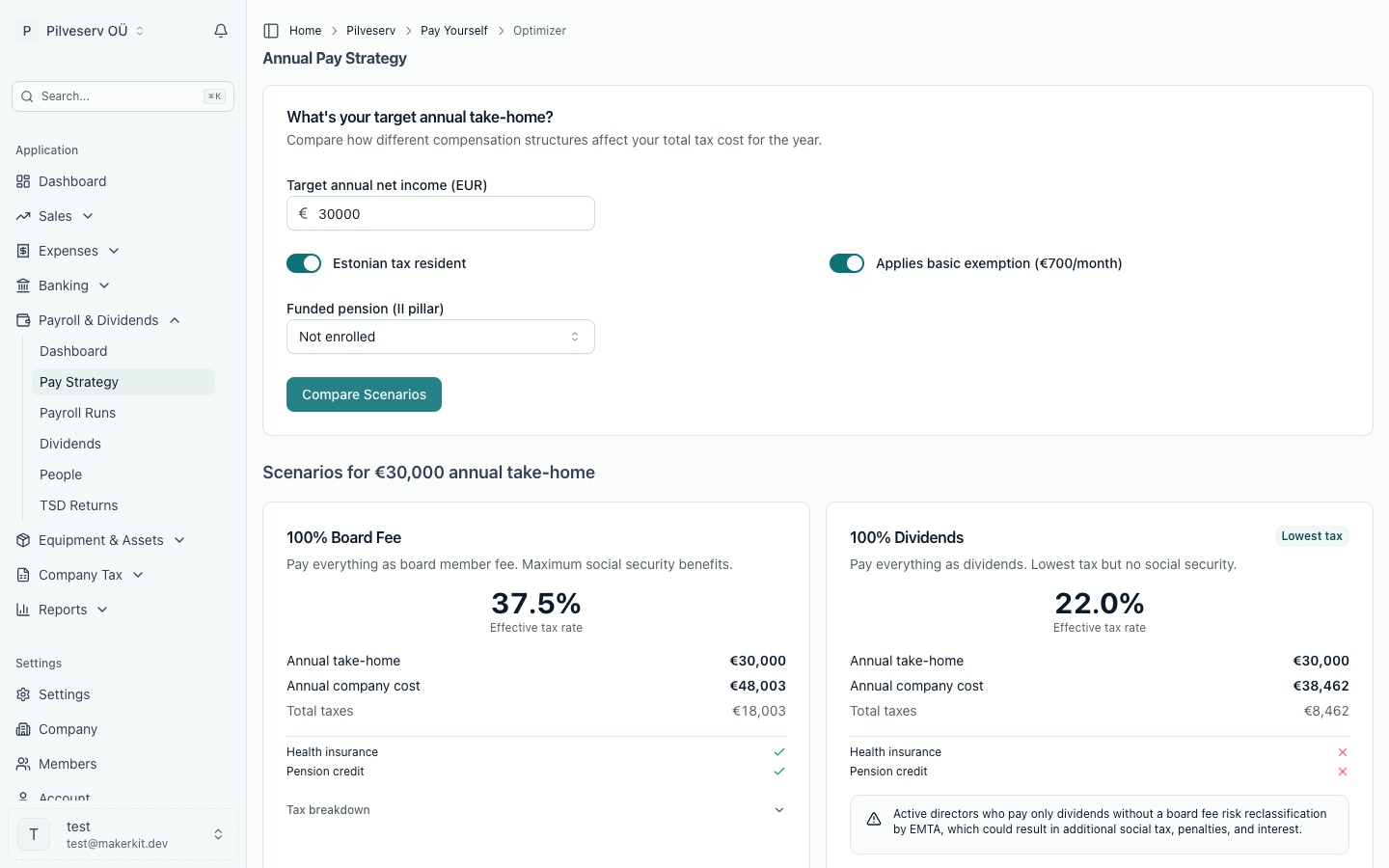

"How should I pay myself?" is the question every OÜ owner asks, and the honest answer is a table, not a slogan. The Pay Strategy page (Payroll & Dividends → Pay Strategy in the sidebar) takes one number — the amount you want to take home in a year — and costs it out four ways, so you can see exactly what each route does to your company's bank account and your own safety net.

The inputs you control

- Target annual net income — what you actually want in hand

- Estonian tax resident — non-residents don't get the basic exemption

- A1 certificate — offered once the resident toggle is off: if another EEA country's social security covers you, Estonian social tax drops out (and so do the health insurance and pension markers)

- Basic exemption — whether the €700/month exemption applies with your company

- II pillar pension rate — 2%, 4%, 6% or not enrolled. This moves the two board-fee routes and nothing else: the contribution is withheld from the board fee (it follows social tax, and board fees are socially taxed), but never from dividends. At 6% the board fee has to be higher to leave you the same amount in hand.

The four scenarios

For a €30,000 annual take-home in 2026 (resident, basic exemption, no A1 certificate, no II pillar), the comparison comes out like this:

| Scenario | Company cost / year | Total taxes | Effective tax rate |

|---|---|---|---|

| 100% board fee (€3,007.69/month gross) | €48,002.76 | €18,002.76 | 37.5% |

| 100% dividends | €38,461.54 | €8,461.54 | 22.0% |

| Min board fee (€886/month) + dividends | €39,600.87 | €9,600.87 | 24.2% |

| Reinvest (take nothing out) | €0 | €0 | 0% |

Each scenario card shows the take-home, the company cost, the tax total, a breakdown by tax type — income tax, social tax, corporate income tax on dividends — and whether the route provides health insurance and pension credit.

How to read it

The numbers say what they say. The lowest total tax cost of the three payout routes is 100% dividends — and it is also the only one that leaves you with no health insurance and no pension accrual, which is why Arvello marks it "Lowest tax" rather than anything warmer. The all-board-fee route costs the most and provides the fullest social-security record. The mixed route — labelled "Most common", because it is — pays a board fee pegged to the minimum social tax base (€886/month in 2026), which keeps social tax flowing and health insurance active for €292.38 of social tax a month, and takes the rest as dividends. Reinvesting defers the question entirely: retained profits carry 0% tax until you eventually distribute them.

The 100%-dividends card carries one more warning worth taking seriously: EMTA, the Estonian Tax and Customs Board, expects active directors to receive a reasonable board fee, and paying only dividends while running the company day-to-day risks reclassification with back-dated social tax, penalties and interest.