Dividends

Estonian OÜ dividend tax explained: corporate income tax at 22/78 on net distributions, calculated by Arvello with the shareholders' resolution generated.

Estonia famously charges 0% corporate income tax on profits you keep in the company. The tax arrives when profit leaves: distribute a dividend and the company pays corporate income tax (CIT) of 22/78 on the net amount handed to shareholders.

Arvello calculates the tax, checks you have profits to distribute, produces the shareholders' resolution document, and puts the distribution on the right month's TSD return.

What's available to distribute

Under Estonian law, dividends can only be paid from profits approved by the shareholders as part of an annual report. The Available for Distribution card on the Pay Yourself dashboard (Payroll & Dividends → Dashboard) therefore counts:

- Retained earnings from prior years, plus

- the profit from your last approved annual report.

Your current year's running profit is shown for information, but it isn't distributable until an annual report covering it has been approved — Arvello reminds you to file the report to unlock it. Both figures come from your accounts; you can see them on the balance sheet. Draft dividends awaiting approval are flagged too, since they'll eat into the same pot.

The tax

CIT is 22/78 of the net distribution, paid by the company on top of what shareholders receive. You can enter either side and Arvello derives the other:

| You enter | Net to shareholders | CIT (22/78 of net) | Gross cost to company |

|---|---|---|---|

| €10,000 net | €10,000.00 | €2,820.51 | €12,820.51 |

| €10,000 gross | €7,800.00 | €2,200.00 | €10,000.00 |

No social tax applies, and since 2025 no further income tax is withheld on regularly taxed dividends paid to resident individuals — the 7% withholding disappeared along with the old reduced rate. (Non-resident shareholders can involve tax treaties; that's one for an advisor.)

Declaring a dividend

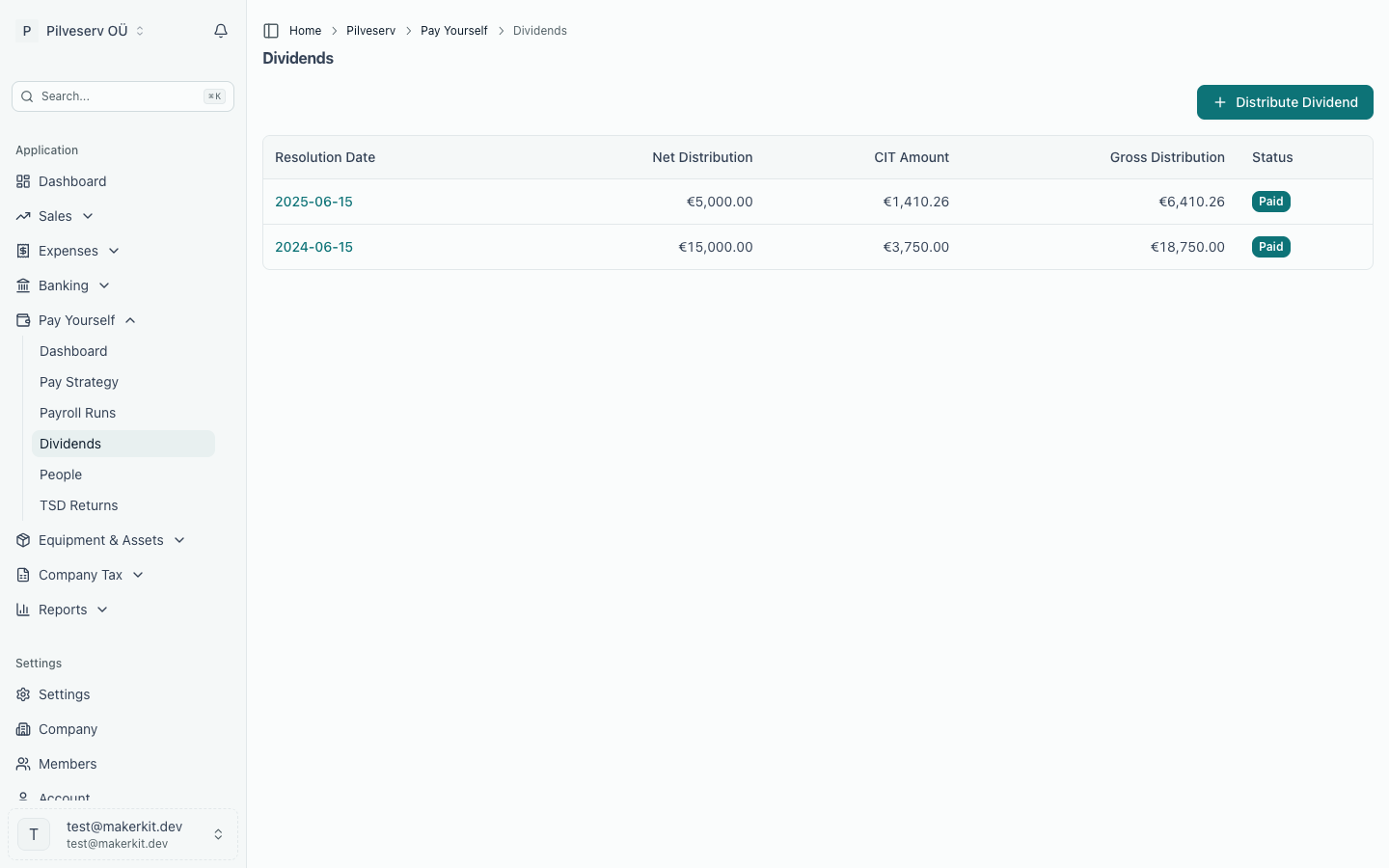

After approval you can Download Decision — a shareholders' resolution PDF in Estonian or English — and mark the distribution as paid once the transfers go out. Every distribution stays in the Dividends list with its resolution date, net, CIT and status, and appears on the following TSD as Annex 7 — see TSD returns.

Dividends versus salary or board fee

The trade-off cuts both ways, so here it is in full:

| Dividend | Salary / board fee | |

|---|---|---|

| Tax cost | CIT 22/78 of net — the lowest total tax cost of the payout routes | Income tax 22% + social tax 33% (+ unemployment insurance on salaries) |

| Social tax | None | 33%, employer-paid |

| Income tax withheld | None on regularly taxed dividends to resident individuals | 22% after any basic exemption |

| Health insurance cover | None — dividends alone leave you uninsured | Yes, via social tax |

| Pension / social-security record | None accrued | Accrues |

| Requires | Approved profits from an annual report | Cash and a payroll run |